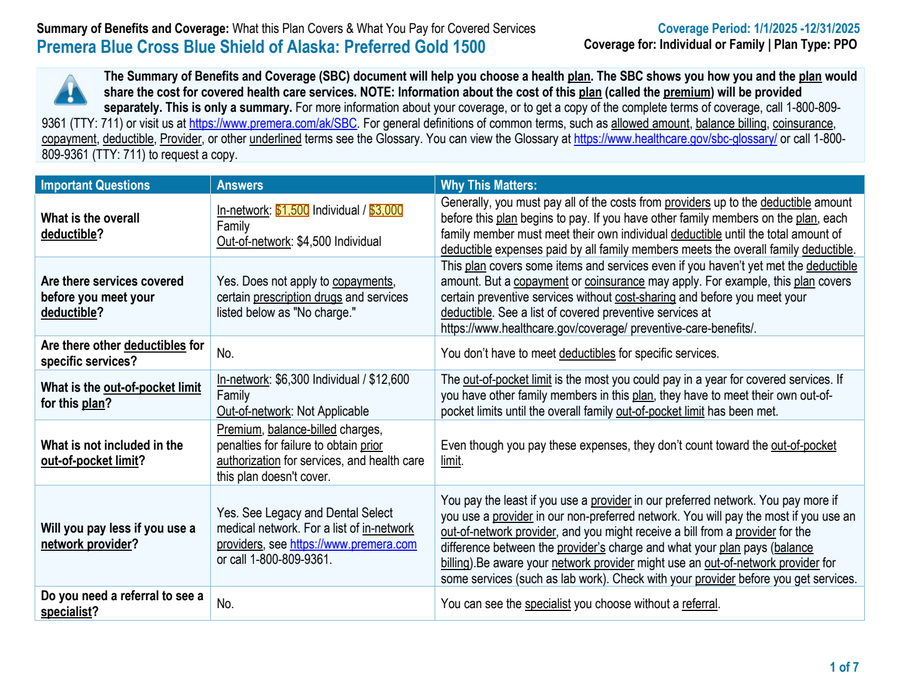

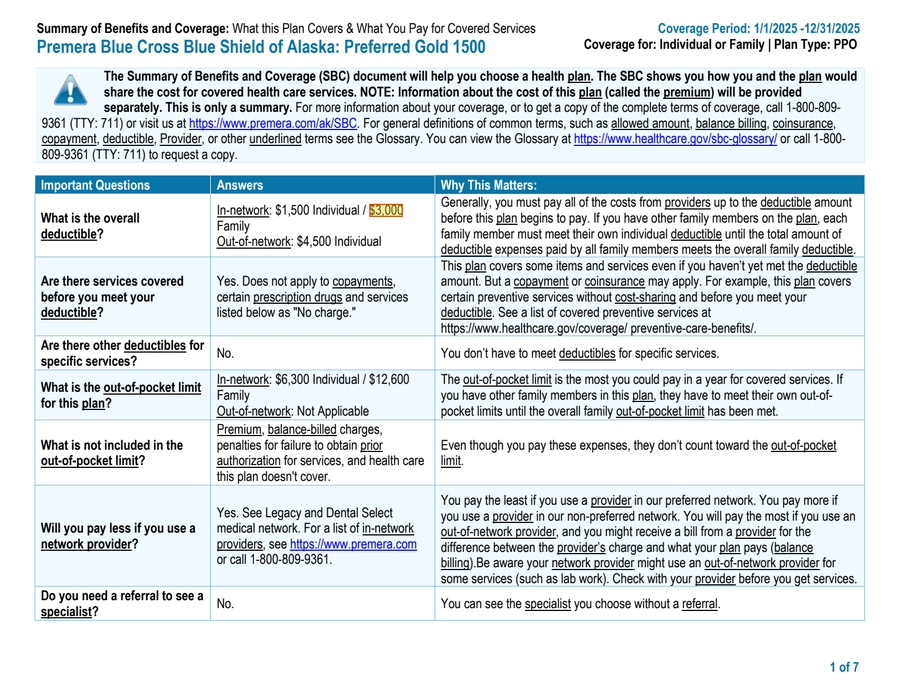

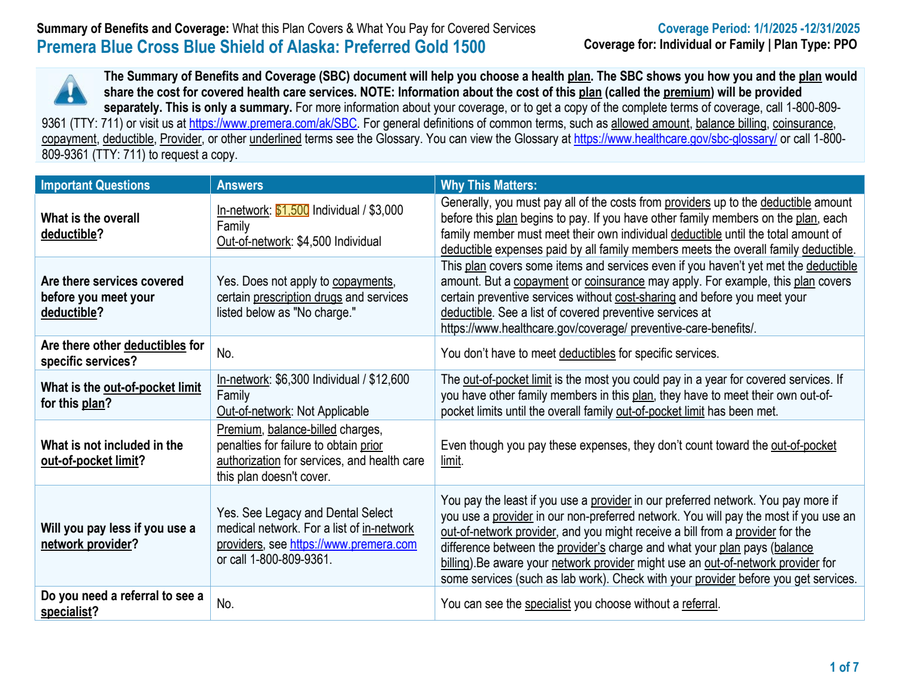

| overall deductible, individual, in-network |

$1,500

p.1

|

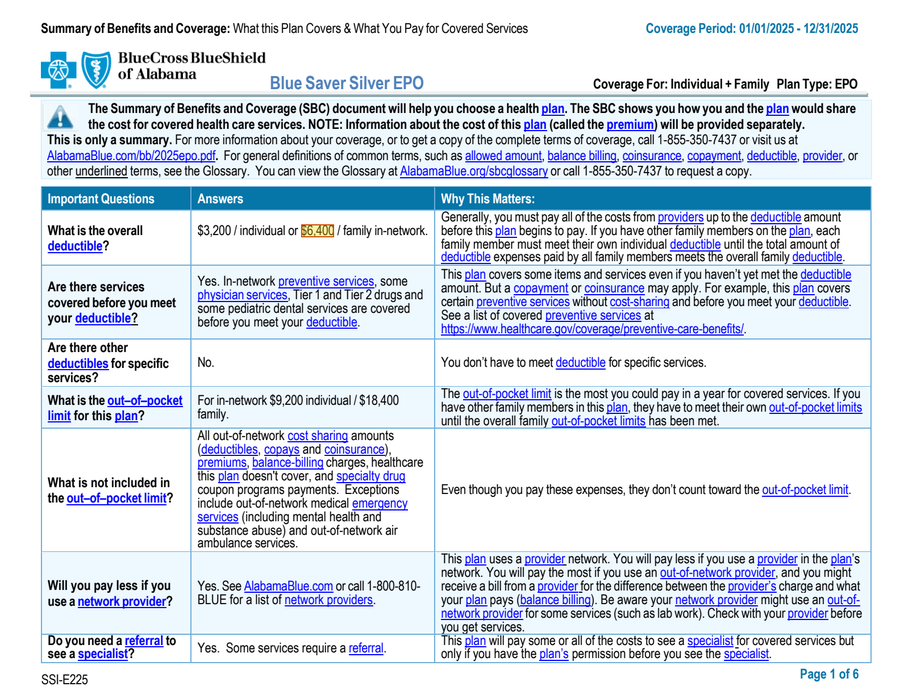

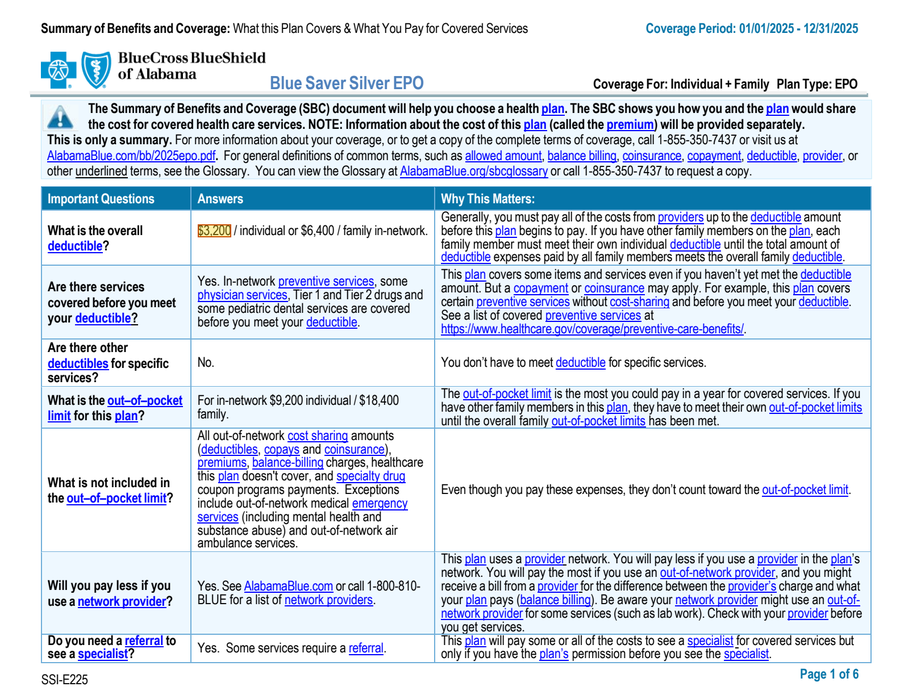

$3,200

p.1

|

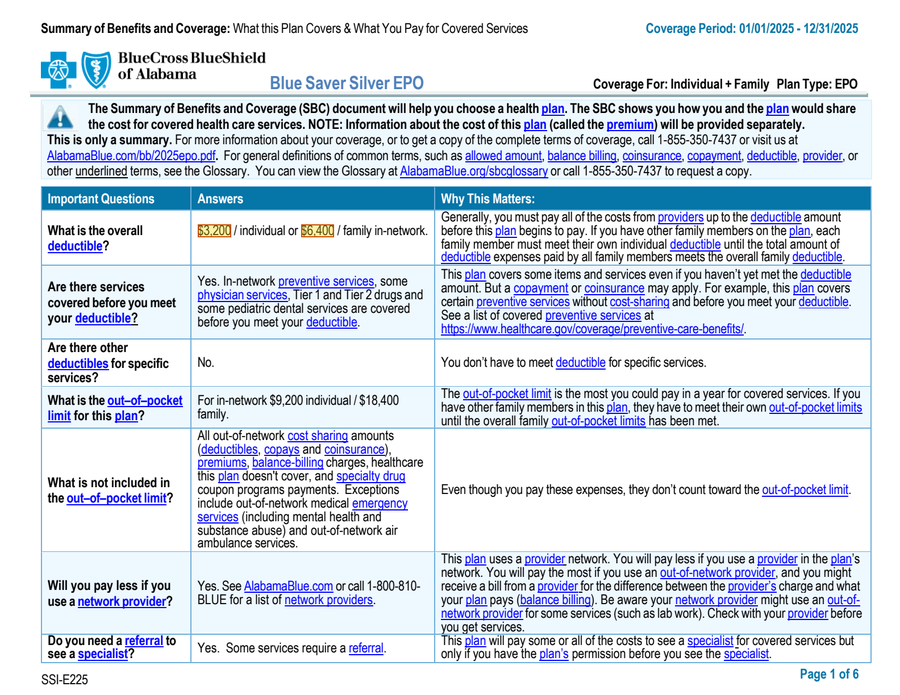

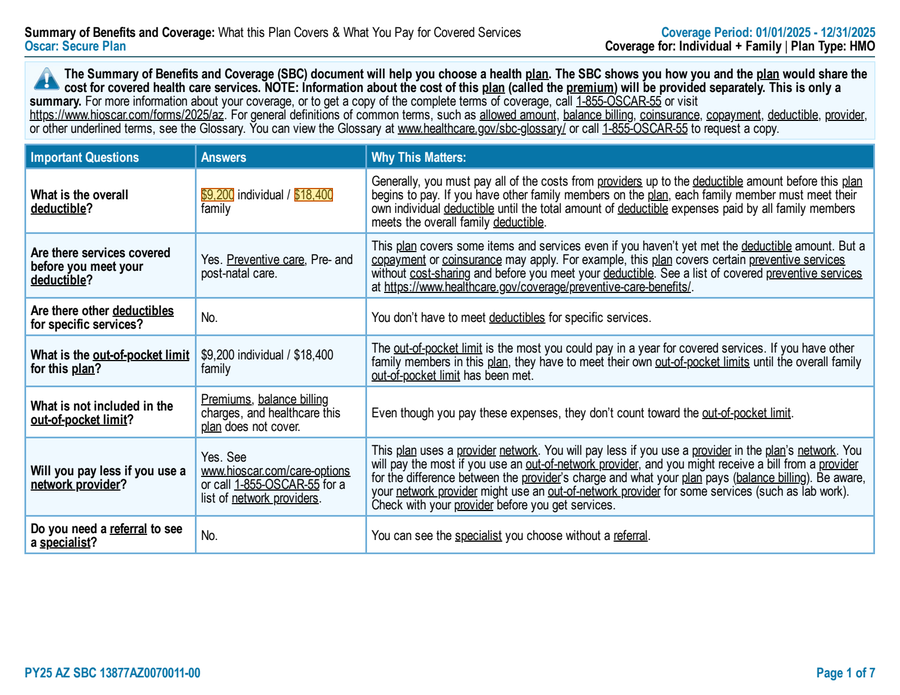

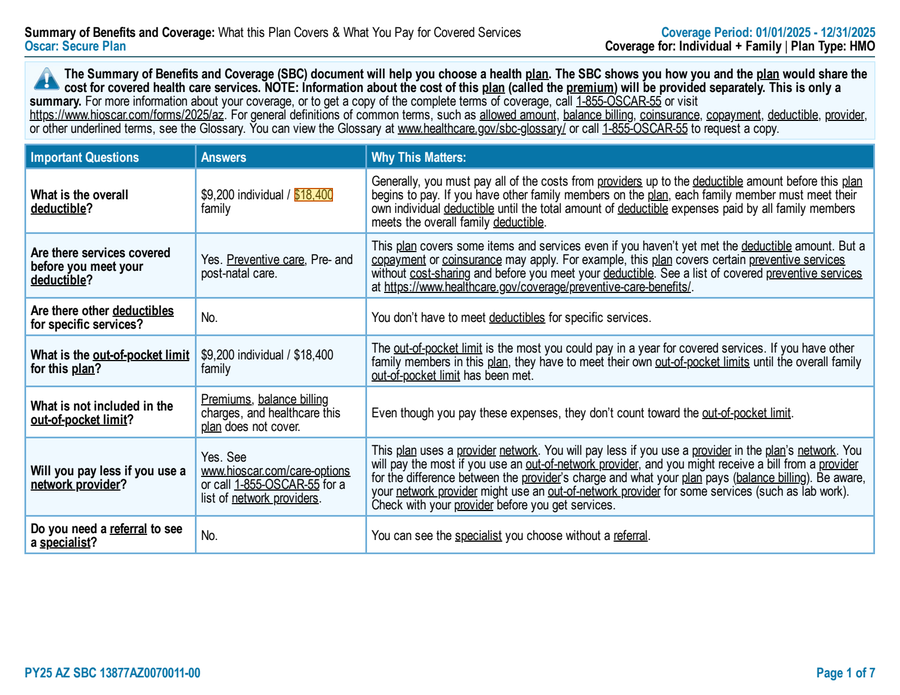

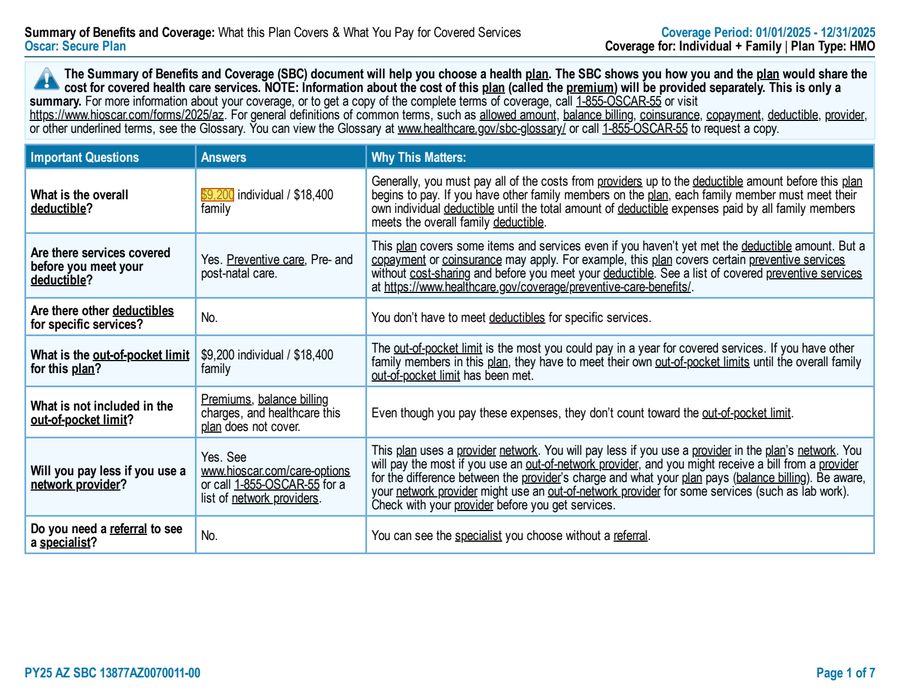

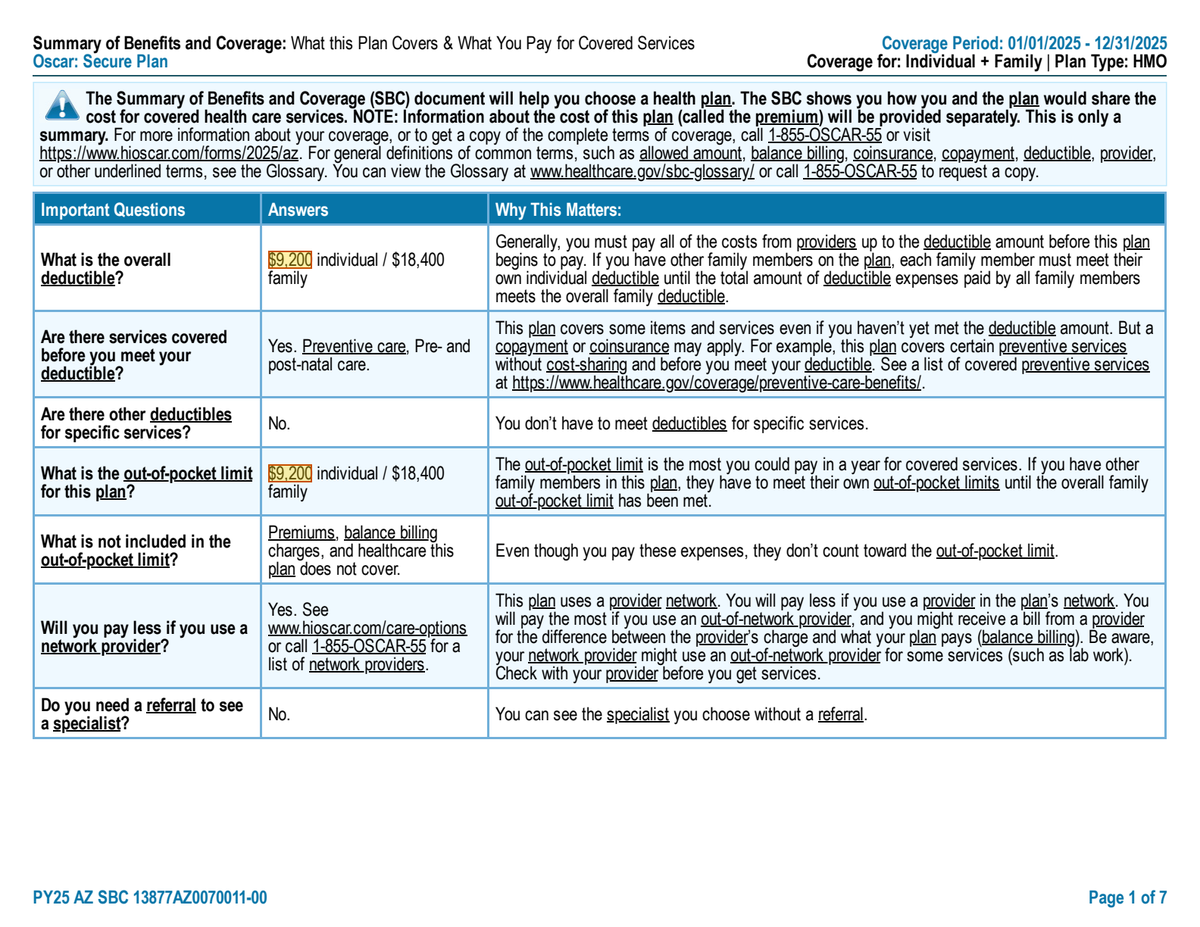

$9,200

p.1

|

| overall deductible, individual, out-of-network |

$4,500

p.1

|

Not Covered

|

Not Covered

|

| overall deductible, family, in-network |

$3,000

p.1

|

$6,400

p.1

|

$18,400

p.1

|

| out of pocket limit, individual, in-network |

$6,300

p.1

|

$9,200

p.1

|

$9,200

p.1

|

| out of pocket limit, individual, out-of-network |

Not Applicable

|

Not Covered

|

Not Covered

|

| out of pocket limit, family, in-network |

$12,600

p.1

|

$18,400

p.1

|

$18,400

p.1

|

| diagnostic test, in-network |

Not applicable

|

25% coinsurance

p.2

|

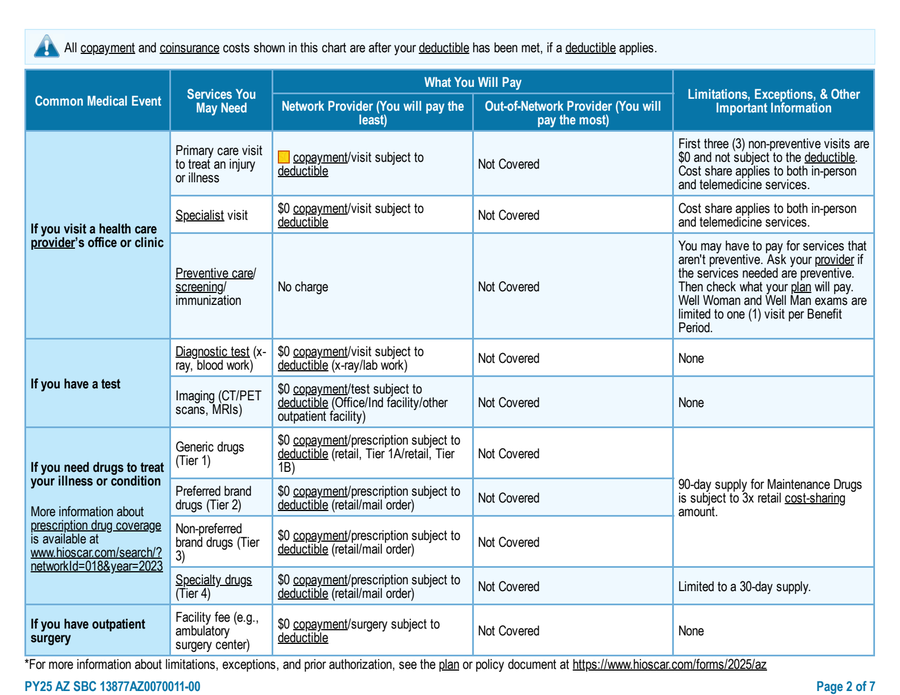

$0 copayment/visit subject to deductible (x-ray/lab work)

p.2

|

| diagnostic test, in-network, participating |

40% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| diagnostic test, in-network, preferred |

30% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| diagnostic test, out-of-network |

Not applicable

|

Not Covered

p.2

|

Not Covered

p.2

|

| diagnostic test, out-of-network, non participating |

Non-Participating: 60% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| drug tier, in-network, tier 1 |

$15 copay / prescription (retail) $45 copay / prescription (mail) Deductible does not apply. $15 copay / prescription (retail)

p.2

|

$5 copay (retail) $12.50 copay (mail order) Deductible does not apply

p.3

|

$0 copayment/prescription subject to deductible (retail, Tier 1A/retail, Tier 1B)

p.2

|

| drug tier, in-network, tier 2 |

$45 copay / prescription (retail) $135 copay / prescription (mail) Deductible does not apply. $45 copay / prescription (retail)

p.2

|

$30 copay (retail) $75 copay (mail order) Deductible does not apply

p.3

|

$0 copayment/prescription subject to deductible (retail/mail order)

p.2

|

| drug tier, in-network, tier 3 |

50% coinsurance 50% coinsurance (retail)

p.3

|

25% coinsurance (retail) 25% coinsurance (mail order)

p.3

|

Not applicable

|

| drug tier, in-network, tier 4 |

40% coinsurance

p.2

|

25% coinsurance (retail) 25% coinsurance (mail order)

p.3

|

$0 copayment/prescription subject to deductible (retail/mail order)

p.2

|

| drug tier, in-network, tier 5 |

Not applicable

|

25% coinsurance (retail)

p.3

|

Not applicable

|

| drug tier, in-network, tier 6 |

Not applicable

|

50% coinsurance (retail)

p.3

|

Not applicable

|

| drug tier, out-of-network, tier 1 |

Not Covered

p.2

|

Not Covered

p.2

|

Not Covered

p.2

|

| drug tier, out-of-network, tier 2 |

Not Covered

p.2

|

Not Covered

p.2

|

Not Covered

p.2

|

| drug tier, out-of-network, tier 3 |

Not Covered

p.2

|

Not Covered

p.2

|

Not applicable

|

| drug tier, out-of-network, tier 4 |

40% coinsurance

p.2

|

Not Covered

p.2

|

Not Covered

p.2

|

| drug tier, out-of-network, tier 5 |

Not applicable

|

Not Covered

p.2

|

Not applicable

|

| drug tier, out-of-network, tier 6 |

Not applicable

|

Not Covered

p.2

|

Not applicable

|

| emergency room care, in-network |

30% coinsurance 30% coinsurance –––––––––––none–––––––––––

p.3

|

Accident: 40% coinsurance Medical Emergency: 40% coinsurance

p.3

|

Not applicable

|

| emergency room care, out-of-network |

Not applicable

|

Accident: 40% coinsurance Medical Emergency: 40% coinsurance

p.3

|

Not applicable

|

| imaging, in-network |

Not applicable

|

25% coinsurance

p.2

|

$0 copayment/test subject to deductible (Office/Ind facility/other outpatient facility)

p.2

|

| imaging, in-network, participating |

40% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| imaging, in-network, preferred |

30% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| imaging, out-of-network |

Not applicable

|

Not Covered

p.2

|

Not Covered

p.2

|

| imaging, out-of-network, non participating |

Non-Participating: 60% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| primary care visit, in-network |

First two visits: $1 copay / visit, deductible does not apply. Additional visits: $30 copay / visit, deductible does not apply.

p.1

|

$10 copay/visit Deductible does not apply

p.2

|

$0 copayment/visit subject to deductible

p.2

|

| primary care visit, out-of-network |

Not applicable

|

Not Covered

p.2

|

Not Covered

p.2

|

| primary care visit, out-of-network, non participating |

Non-Participating: 60% coinsurance

p.2

|

Not applicable

|

Not applicable

|

| prior authorization penalty |

$1,500 per occurrence

p.1

|

see penalty text

p.2

|

Not applicable

|

| specialist visit, in-network |

$60 copay / visit, deductible does not apply.

p.2

|

$90 copay/visit Deductible does not apply

p.2

|

$0 copayment/visit subject to deductible

p.2

|

| specialist visit, out-of-network |

Not applicable

|

Not Covered

p.2

|

Not Covered

p.2

|

| specialist visit, out-of-network, non participating |

Non-Participating: 60% coinsurance

p.2

|

Not applicable

|

Not applicable

|